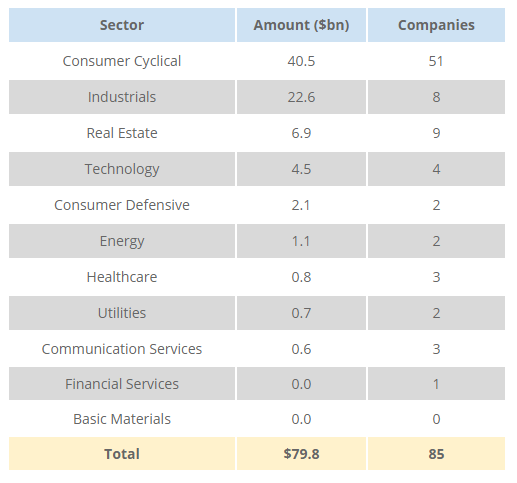

Updated on 3/31/2020 for additional data from algorithm refinement As social distancing and business closures have taken hold in the last several weeks in response to the developing Covid-19 pandemic, a number of companies are bracing for a downturn by improving their liquidity ... >>>Read More

Share Repurchase Strategies for Volatile Markets

Over the past three weeks, the VIX index (a measure of expected volatility of the US market over a 30-day forward looking period) has steadily increased from the mid teens to a maximum of 82.7% on 16-Mar-2020. To put this in perspective, the VIX index peaked at 80.9% during the 2008 financial ... >>>Read More

Measuring COVID-19’s Impact to the Convertible Market

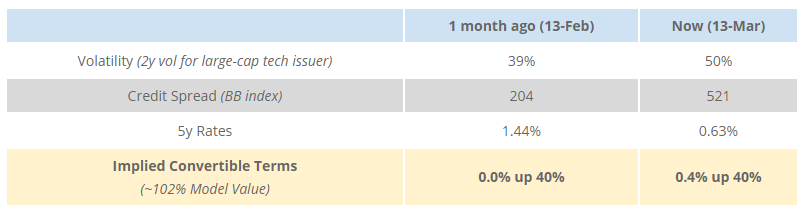

Over the past three weeks, prospective issuers have heard versions of the following banker simplification of the convertible market: “Convertible pricing is very attractive because rates are at historic lows and the benefit from the increased volatility offsets widening credit spreads.” While ... >>>Read More

February Convertible Market Review

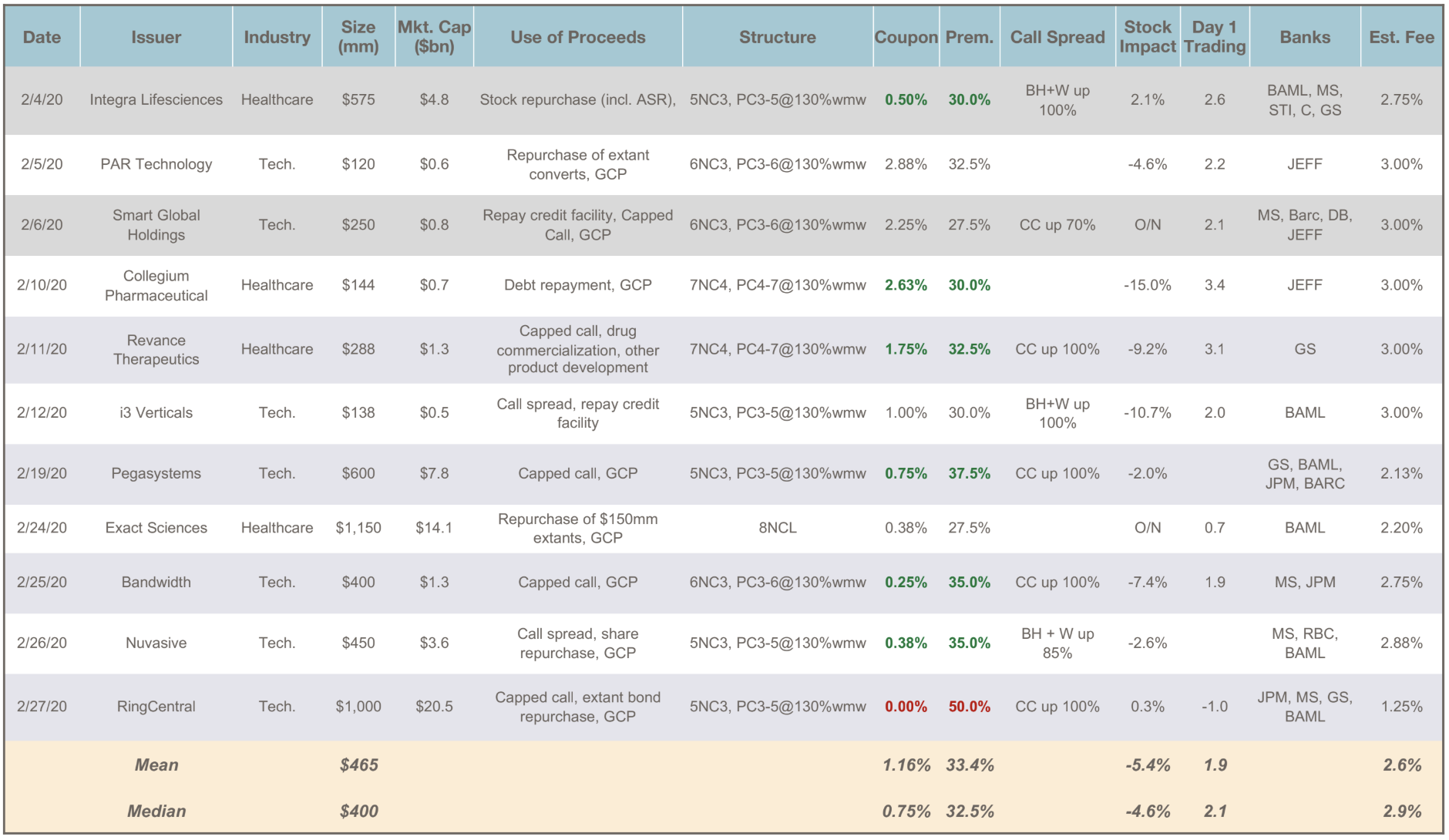

Total Issuance: Despite the sharp market sell-off, February was a very busy month in the convertible market. A total of $5.1 billion priced over 11 deals – a higher dollar volume than every month of 2019 except for August and September. Activity was in fact concentrated (4 deals for ... >>>Read More

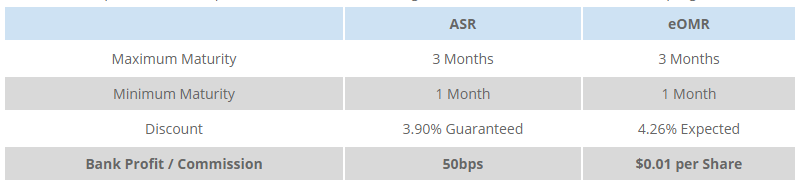

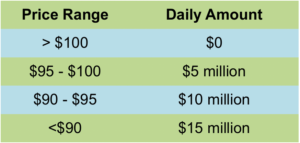

A better way to assess OMR broker performance

Companies in the S&P 500 alone spent $770 billion in the past four quarters on share repurchase. The majority of this buyback was executed through open market repurchases (“OMR”), including 10b5-1 plans. In OMR programs, the broker, as an agent of the company, executes the ... >>>Read More

- « Previous Page

- 1

- …

- 5

- 6

- 7

- 8

- 9

- …

- 12

- Next Page »